What Are The Insurance Requirements for Office Space Tenants?

Office Insurance

All companies should have insurance coverage to shield against legal pitfalls. When leasing office space, insurance acts as a safety net, protecting both the tenant and landlord against property damage and personal injuries. It also ensures compliance with legal requirements, including worker compensation mandates.

Landlords require tenants to carry insurance policies that offer specific coverage amounts. These amounts may vary from building to building and by the size of office space leased. Presenting your company's Certificate of Insurance—often referred to simply as a COI—to the landlord is usually the final step before the landlord hands over the keys to the office, providing a sense of security for both parties.

Ensure that your office is safeguarded against the unexpected.

Understanding the Basics of Office Space Insurance

Before a landlord allows a company to take possession of their new office space, the landlord must ensure the company is adequately insured. Specifically, when the landlord hands over the keys, the company must have a general liability insurance policy in place. This policy protects both the new tenant and the landlord against accidents that occur at the office. If your client slips on a banana peel and ends up in traction, you're both covered.

The insurance section of the master lease outlines the specific coverage required. Understanding this section is key as it can help you negotiate better terms and avoid potential issues. If the coverage amounts are deemed onerous, a tenant's real estate attorney or broker may ask to reduce them.

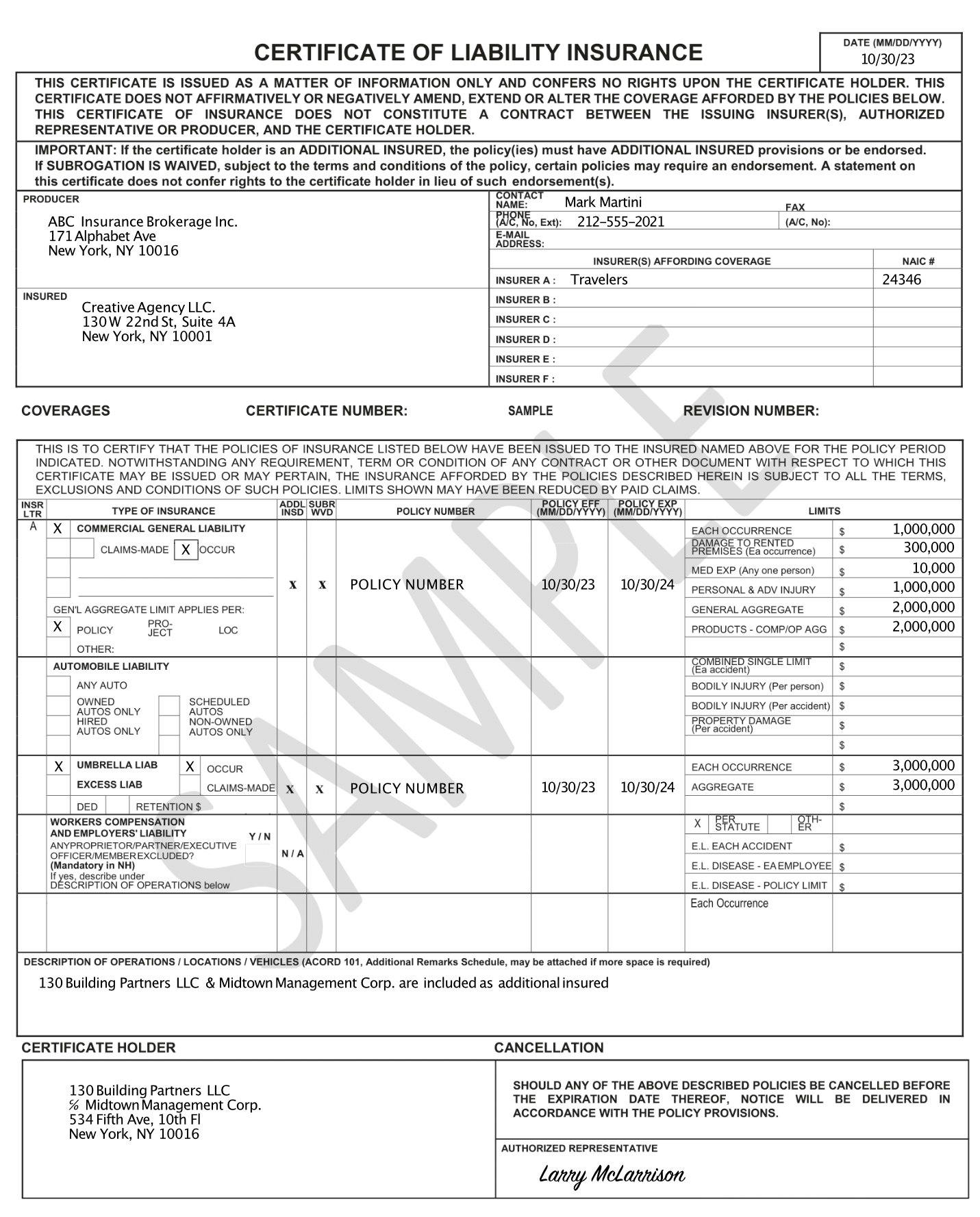

It might initially look confusing if you've never seen a Certificate of Insurance. The one-page document contains a lot of information.

Bob's spill on a banana peel turned comedy into claim.

If you get hurt and miss work, it won't hurt to miss work.

The sections of a typical COI:

Producer - The 'Producer' section of the COI lists the name, address, and contact information of the insurance agency and/or broker that issued the certificate. This section provides the insured party, the insurer, and third parties requiring proof of insurance with a point of contact to verify the COI's authenticity and coverage.

Insured - The 'Insured' section identifies the policyholder—the individual or entity covered by the insurance policies listed on the certificate. It includes the insured's name and address. This section allows third parties to verify that the entity they are engaging with has the necessary insurance protection.

Additional Insured - The 'Additional Insured' section specifies any other parties, besides the policyholder, who are covered under the insurance policy and require protection against liabilities arising from the policyholder's operations. Being listed as an additional insured extends certain coverages to landlords and their various legal entities. This designation is common when additional parties need coverage under the policyholder's insurance for the duration of a lease.

Certificate Holder - The 'Certificate Holder' section names the entity that receives the certificate and has a vested interest in knowing about the insurance coverages in place. Regarding office insurance, this would be the landlord's company. It lists their name and address, which confirms their right to receive notifications about any changes to the policy.

Coverages - The 'Coverages' section outlines the specific types of insurance policies the insured has, such as general liability, auto liability, workers' compensation, and professional liability. It details the scope of protection provided, including policy numbers, effective dates, and coverage limits.

General Liability - The 'General Liability' section details coverage that protects the insured against claims involving bodily injury and property damage arising from their daily operations, products, or premises. For landlords—the certificate holders—this section confirms that the insured has basic coverage for accidents that could occur in the office building.

Worker's Compensation - The 'Workers' Compensation' section specifies coverage for employees who get injured or sick from a work-related cause. It outlines the extent of protection for medical costs, lost wages, and rehabilitation expenses and safeguards the insured against financial liabilities from employee claims.

Umbrella Policy - An umbrella policy provides additional protection beyond the limits of underlying policies. Its coverage kicks in once the limits of the underlying policies have been reached, offering an extra layer of financial security to the insured. Opting for an umbrella policy instead of simply raising the limits of the specific policies is often a matter of cost efficiency and broader scope of coverage. By broadening coverage, an umbrella may include claims not covered under the primary policies. Managing one umbrella policy that extends over several underlying policies (like auto, employers' liability, and general liability) can simplify administration and ensure consistency in coverage.

Excess Liability - 'Excess Liability' provides additional limits above the insured's primary liability policies. Unlike umbrella liability, excess liability typically does not broaden the coverage but instead increases the monetary limits of the underlying policies. Both excess policies and umbrella policies increase protection; however, excess liability is more narrow in focus because it only extends the limits for specific, already-covered risks, while umbrella liability offers both an increase in limits and a broadening of coverage.

Certificate of Insurance (COI)

Navigating the landlord's insurance requirements can be confusing, especially for companies renting office space for the first time. However, you're not alone; your office broker will be there to guide you every step of the way, which may include referring you to an insurance agent. This will help you secure adequate coverage, satisfy lease obligations, and offer protection against possible liabilities.

Before your company takes occupancy of a new office, remember that the Certificate of Insurance is required. It's crucial to review and understand the coverage details, as this knowledge empowers you to protect your business from unforeseen events. Work with a knowledgeable insurance broker to tailor a policy that fits your company's specific needs. These steps can give you the confidence to navigate the insurance process effectively.